[PRESS RELEASE] High Street exits remain at historic high as openings slump to lowest levels on record - What now for retailers?

Date published: 2019-04-10 Date modified: 2023-08-16

-

Largest full year net decline in stores as deficit breaches 2,400 for the first time

-

16 stores a day closing, as increasing cost of occupancy, shift to online and subdued consumer spending take their toll

-

Store openings drop to 9 a day - almost half the levels of 5 years ago - due to structural changes in consumer habits

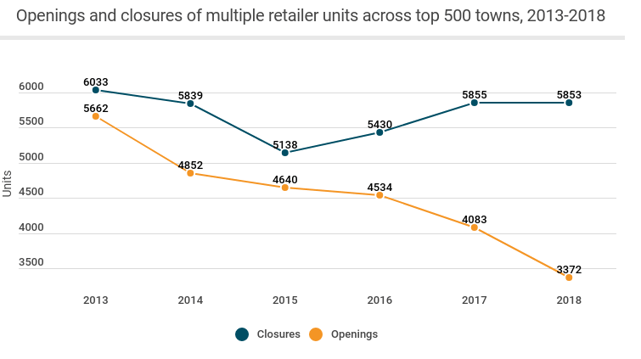

The number of store openings by multiple retailers on Great Britain’s top 500 high streets has dropped by 17.4% year on year with the current rate of openings at nine stores per day. This also represents a 44% decrease from the 16 stores per day opening in 2013 (See Figure 1).

Relative to 2017, the rate of store closures in 2018 remained at 16 stores a day. However, the shortfall between openings and closures reached its highest level since the beginning of the decade, as withdrawals from the high street were further dented by a historic low number of store openings.

Figure 1. Openings and closures of multiple retailer units, 2013-2018 (Source: Local Data Company).

Lisa Hooker, Consumer Markets Leader at PwC, said:

“The results are clear - 2018 was a turbulent year for retailers with a number of high profile store closures. We saw an acceleration in footfall decline on the high street with businesses continuing to see the impact of online shopping, increasing costs and subdued consumer spending.

“It’s interesting that the marked reduction in openings has accelerated the net closure trend. In categories as diverse as fashion and financial services, new entrants are able to gain share by launching online - enabled by technology and consumer adoption of mobile and e-commerce - rather than be saddled with the costs and risks of opening on the high street.

“The high street of the future will be a more diverse space, not solely dependent on stores. The analysis reflects this with the net growth of gyms and sports clubs, ice cream parlours and cake shops, in addition to initiatives to bring more shared office spaces and homes into what were traditionally shopping areas. However, it’s clear that the rate of openings is not currently enough to offset the closure of traditional retailers and services, so some tough decisions will need to be taken in the next few years.”

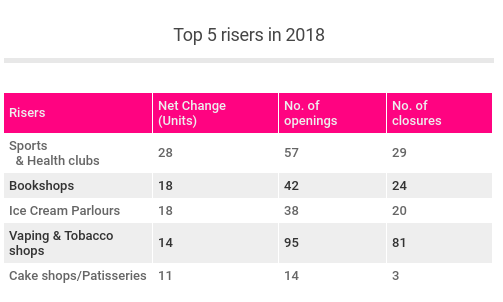

Table 1. Top 5 net risers in 2018 (Source: Local Data Company).

On a category basis, only 15 out of 100 business types showed a net growth in outlets numbers, and only five categories showed net growth in double digits (See Table 1). Categories traditionally amongst the risers in previous years, such as coffee shops, food to go, takeaways, jewellers and beauty shops, have all seen net declines in 2018 as overcapacity and economic conditions took their toll.

The roll out of gyms leads the growth categories, as high streets begin to pivot away from retail; while other growth categories were dominated by entertainment and indulgence with bookshops, ice cream parlours and cake shops all in the top five.

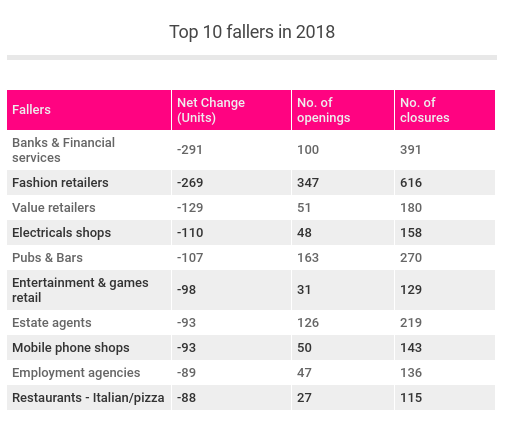

Conversely, the top 10 declining business types are dominated by retailers and service businesses, most impacted by the shift to online (See Table 2). These include fashion and electrical retailers, many of which have lost share to prominent online retailers.

In addition, traditionally store-based services such as banks, estate agents and recruitment agencies, whose business is also increasingly undertaken remotely have all figured heavily. These three categories alone accounted for a net 473 store reduction in presence on the UK’s 500 largest high streets in the last year.

Table 2. Top 10 net fallers by business type in 2018 (Source: Local Data Company).

The analysis also observed a slowdown in leisure, in particular restaurants and pubs, which posted a net loss of 506 outlets, reversing three years of consecutive growth since 2015. Market saturation, cost challenges, and a shift in consumer preferences towards in-home leisure have exacerbated the impact on the sector, not only leading to closures but also discouraging new openings.

Looking at the first quarter of 2019, Local Data Company data finds that closure rates remain high as 1,358 outlets alongside 849 openings. This is a direct consequence of CVAs, store downsizing and administrations announced in 2018 feeding through across GB.

Zelf Hussain, retail restructuring partner at PwC, said:

“Several national chains weathered company voluntary arrangements or administrations as retailers toiled in the tough climate of 2018. Retail companies looking to survive let alone flourish in 2019 face an uphill battle.

"We have already seen several casualties in 2019 and there will undoubtedly be more, most likely in all categories except for groceries. Those retailers who will give themselves the best chance of survival must focus on having the relevant proposition, and the investments needed to deliver this proposition; the optimal mix of channels and business portfolio; flexible leases.

"Additionally, we believe CVAs are not the answer in isolation. Companies need solutions that fully address customer needs, represent sustainable cost savings and, if needed new money investment to bridge the lag between the cost of a restructuring and long-term performance improvements.”

Across regions and nations...

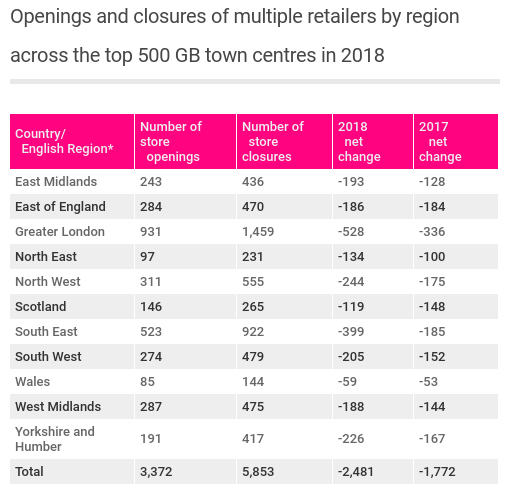

Table 3. Openings and closures of multiple retailers by region across the top 500 GB town centres in 2018 (Source: Local Data Company).

Table 3. Openings and closures of multiple retailers by region across the top 500 GB town centres in 2018 (Source: Local Data Company).

Greater London saw the largest number of net closures across all the regions, with fashion retailers closing the most in the capital (-79 units). Scotland was the only region to see a drop in its net closures, dropping from -148 in 2017 to -119 in 2018. Wales was the best performing region, posting the lowest overall net decrease in chains of - 59.

Lucy Stainton, Head of Retail and Strategic Partnerships at the Local Data Company, said:

“A key trend from this latest analysis is the increased loss in leisure units across the top 500 towns. We identified the start of this decline in H2 last year and sadly this has worsened due to an incredibly competitive marketplace and rising operating costs. We anticipate further losses in the leisure sector as brands which fail to entice customers to spend across multiple trading periods -breakfast, lunch and evening- close stores for good.

“Also key to note is that the two regions that were previously less susceptible to market challenges, Greater London and the South East, are now the two that have been hit the hardest by store closures.

“However, there are still green shoots breathing life into this sector with brands trialing new grab-and-go concepts. It will be increasingly important for leisure operators to be agile to keep their offer relevant. Bricks and mortar has a strong future- but not as we know it. Stores and shopping destinations will continue evolving to better serve consumer demand, integrating as part of an online channel.”

ENDS

For all press enquiries please contact david.jetuah@pwc.com.

Author

PwC and the Local Data Company

The Local Data Company

901

901

901

901

Local Data Company is the UK’s most accurate retail location insight company. We physically track every retail and leisure business across the entire country. Our data powers strategy and decision making for our clients working across retail, leisure, out-of-home media, investment, property and financial services.