Growth and Decline: Exploring the Surge of Barbers and the Decline of Pubs

Date published: 2024-04-03 Date modified: 2024-04-10

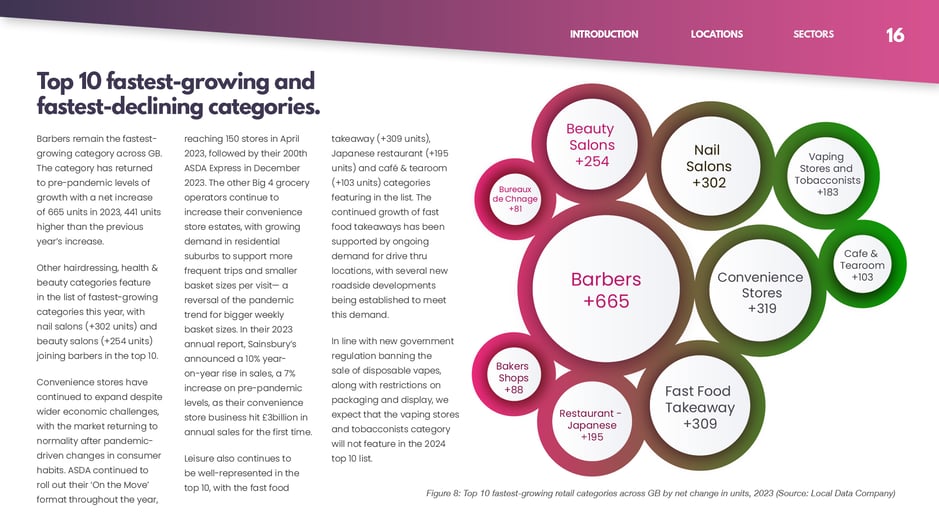

The latest report by the Local Data Company and Green Street covers key developments across the entire GB retail and leisure market over 2023. Our new retail and leisure research shows a spike in numbers of both closures and openings, representing significant churn. We did a deep dive into these fastest-growing category and the fastest declining-category in terms of access to these services by population. Barber remained the fastest-growing category across GB, reflecting sustained demand for personal grooming services.

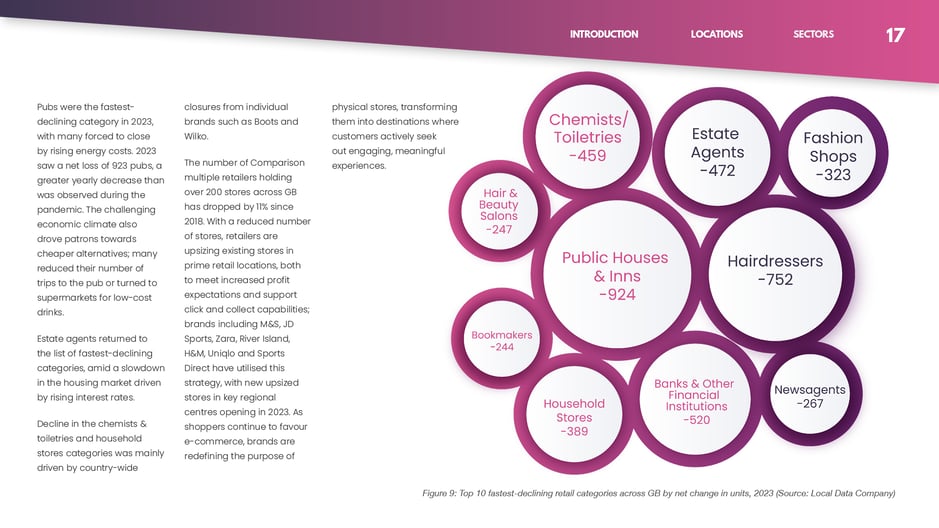

A common denominator for the sectors who are most affected by closures, are the high energy prices the UK. Due to the challenging economic climate for both operators and consumers, resulting in pubs becoming the fastest-declining category in 2023.

Barbers

With barbers taking the top spot in terms of net unit growth for the past few years, what does this look like when compared to the population of England & Wales.

Barbers per Capita 2013 Barbers per Capita 2023

The average number of Barbers per 10,000 people has more than doubled in the last 10 years, going from 1.4 per 10,000 people to 3.1 in 2023.

Areas around London and many areas in the North have seen the biggest increases with 19 Local Authorities having more than 4 Barber Shops per 10,000 people in 2023.

Pubs

Pubs saw the biggest net decline in units in 2023 with a net loss of 924 units mainly caused by economic factors such as the cost-of-living impacts on consumer spending.

Pubs per Capita 2013 Pubs per Capita 2023

However, when looking at the numbers over the past decade, the number of pubs per 10,000 people in England & Wales has increased from 3.0 in 2013 to 3.8 in 2023.

Areas in the North and Midlands have seen the biggest increases. However, it remains to be seen how the leisure industry will fare in 2024 in this turbulent trading environment of late.

To read more about key developments across the entire GB retail and leisure market over the past year, download the Local Data Company's new FY 2023 report with insights from parent company Green Street.

Author

Hayley Kennedy

The Local Data Company

901

901

901

901

After completing her degree in Retail, Marketing & Management, Hayley went on to build a successful career between 2009 and 2019 as a merchandiser working for established retailers such as Arcadia and The White Company. Her last two roles at The White Company and Soho House (Cowshed) were maternity cover contracts and, because of her career moves, she is highly adaptable. A vast proportion of Hayley's role as Merchandiser was dedicated to numbers: data collection and data analysis working with raw data focused on stores, individual products, product lines, stock management, sales and returns.