WHERE WILL COVID-19 LEAVE THE RETAIL AND LEISURE MARKET AT THE END OF 2020?

Date published: 2020-11-19 Date modified: 2023-08-16

As we move towards the end of the year, the 'golden quarter' hasn't quite felt like the festive frenzy that many occupiers rely on to boost revenue. Rising COVID-19 cases and deaths and a second national lockdown has resulted in a more sombre start to Christmas, which many had not anticipated.

We recently released our H1 2020 retail and leisure market update which provided a detailed overview of how the market changed over the first half of the year. Within the report, we included forecasts of where we think we could be at the end of this year (which alarmingly falls just 6 weeks away today). Using Local Data Company data collected since 2013 alongside modelling techniques we were able to make estimations for what the COVID-19 pandemic may leave the GB retail and leisure market.

Openings and closures

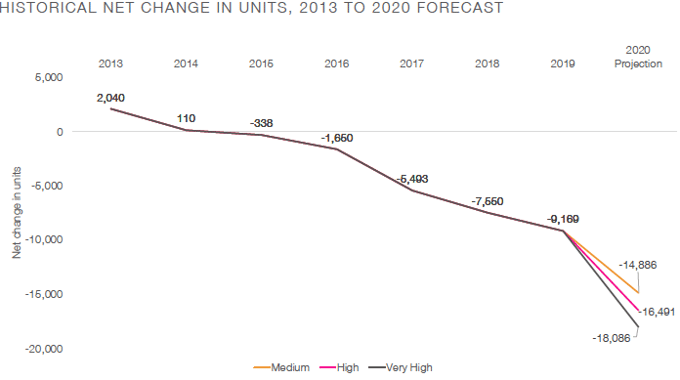

Our analysis considered several factors and likely outcomes to generate projections on the number of openings and closures we expect in 2020. Factors included the level of churn that has occurred in the year so far, data from September and October and the potential impact of further government interventions (i.e lockdown). Considering these factors, we explore three different scenarios: best case (medium risk), medium case (high risk) and worst case (high risk), dependent on the continually changing market landscape.

Each forecasted scenario would see a record level of net closures in the year with the best case a decline of -14,886 units. This would result in a 62% increase on the net decline seen in 2019, and factors in the likelihood that many retailers are hope to trade through what is left of the Christmas period waiting to review their property portfolio in the new year. We forecast some opening activity from retailers looking to do deals and use the availability of property to grab prime pitch space and realign their portfolio to the new climate.

Forecasted net change in occupied units across GB, 2013 to 2020 (Source: Local Data Company)

Buckle up - the worst-case scenario was based on outcomes if a second nationwide lockdown was imposed across the country - which we are now right in the middle of. Lockdown 2.0 was imposed after months of the 10pm curfew, which caused havoc for the hospitality sector, causing big names such as Cineworld to temporarily close cinemas back in October due to the low levels of footfall and lack of major box office releases. Odeon and Vue followed suit cutting their trading hours.

This worst case scenario also considers the continued migration of spend from physical stores to online channels, leading to comparison retailers closing bricks and mortar stores in order to adapt to a digitally-led future. Several CVA proposals are also filtering through, causing increased volumes of store closures.

Vacancy

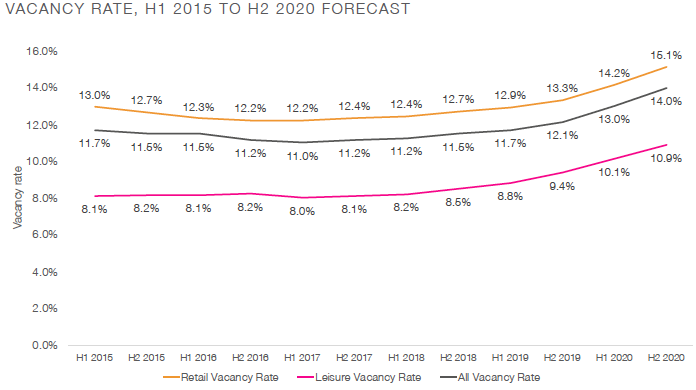

Taking the current trajectory and the above forecast into account, we anticipate GB vacancy could reach 14% by the end of 2020 - a 1% increase from H1 2020. This would represent the biggest increase between half years since we started tracking this metric.

One might expect this to be higher, but less churn is commonly seen at the end of the year as operators focus on Christmas trading opportunities. As government support changes, and furlough winds down (possibly) in March next year, chains are likely to announce further redundancies and store closures. This has already started with Burger King, TSB, H&M and Pizza Hut making announcements at the end of September. CVAs will flood into the market as the deadline for moratorium on forfeiture of commercial leases for non-payment approaches, leading to tough decisions being made about stores that remain closed since the first lockdown came into effect in March.

Forecasted vacancy rate by retail type across GB, H2 2020 (Source: Local Data Company)

reopening rates

A key COVID-19 metric we have been tracking is the rate at which the non-essential market opened back up after the first lockdown.

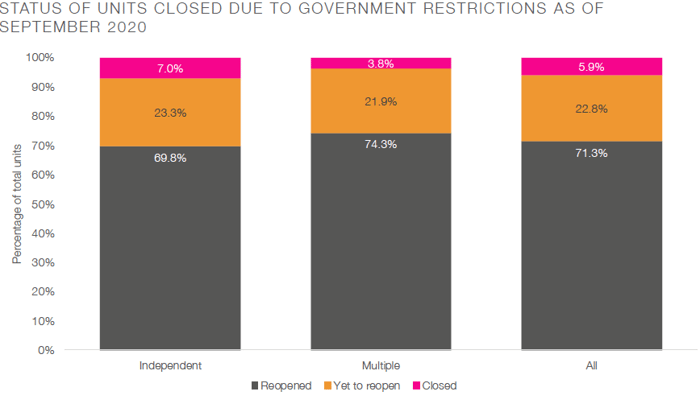

At the end of August, reopening rates across England had reached 71.3%, leaving 22.8% of units still temporarily closed and 5.9% vacant. Multiples were faster to recover with a reopening rate of 74.3%, boosted by their ability to raise capital supporting survival during lockdown.

Independents were less likely to get access to capital but would have been able to take advantage of government support packages such as furlough and business rates relief, which would have helped them to preserve cash. This has resulted in a larger percentage of independent units surviving, but unable to reopen due to the difficulty in making stores compliant with COVID-19 guidelines and smaller square footage making social distancing tricky.

Current status of units that closed during lockdown across England as of September 2020 (Source: Local Data Company)

Current status of units that closed during lockdown across England as of September 2020 (Source: Local Data Company)

We anticipate that the majority of units that had not reopened after the initial lockdown will not do so now. If 70% of the units still shut failed to reopen this would result in 21% of units that closed for lockdown shutting forever.

A more conservative picture might be just 45% of the units yet to reopen closing permanently, which would result in 15% of all units that closed for lockdown being vacated. Both forecasts require a long-term solution that would give retailers confidence of some level of normality returning with fewer local lockdowns, office workers returning to city centres and international tourists feeling safe to travel to the UK.

reSIZING THE retail property MARKET

In 2019, 8.7% of the vacant units at the start of the year were taken out of the retail market either seeing structural change (merged, split, demolished) or were converted into other asset classes such as office and residential. In order to manage an inevitable rush of closures early next year, landlords will have to make tough decisions about their retail assets. For councils and BIDS, towns that pre-COVID-19 had a vacancy rate above the GB average are the most exposed and should be urgently reviewing how property is being utilised within their locality.

The volume of redevelopment needed in the market in 2021 much surpass that seen in 2019, given the scale of the problem on the horizon. With vacancy likely to reach the late teens by H1 2021, there will be an urgent requirement to convert around 15% of retail space into residential or other uses in order to rebalance our high streets.

This resizing of the market is a painful yet critical step towards reshaping UK high streets into diverse, thriving and functional locations, which are convenient and enjoyed by the surrounding population.

Author

Ronald Nyakairu, LDC Senior Manager- Insight & Analytics

The Local Data Company

901

901

901

901

Ronald has a Masters Degree in Business Analytics which focused on the analysis of consumer habits in the tourism sector. He has worked at the Local Data Company since 2014 and now heads up the insight team which supports our retailer, property, landlord and local authority client base. he has worked on projects on retail redevelopments, planning proposals and appeals, due diligence, pre-acquisition due diligence, market studies and investor strategy. He also works closely with our academic partners at five universities, supporting the development of new research in the retail sector, as well as supporting over 40 PhD, Masters and Graduate students. He has regularly contributed to media coverage and has featured in the FT, The Telegraph, The Guardian and The Sunday Times, as well as speaking at events for Retail Week, Blackrock and RPA.